Introduction

June 2026 was a month of quiet transition for the global pigment and coatings industry. Titanium dioxide prices diverged sharply by region, large-scale consolidation among coatings majors continued to move through regulatory approval, and ocean freight markets entered what logistics providers are calling a “turning point” between a stable first half and a more volatile Q3 peak season. On the regulatory front, Europe’s sweeping PFAS restriction proposal cleared another procedural milestone, while Brussels quietly shelved its broader REACH revision plan — a small but meaningful reprieve for manufacturers. Below is our roundup of the developments that mattered most to pigment producers, buyers, and formulators this month.

1. Market & Price Trends

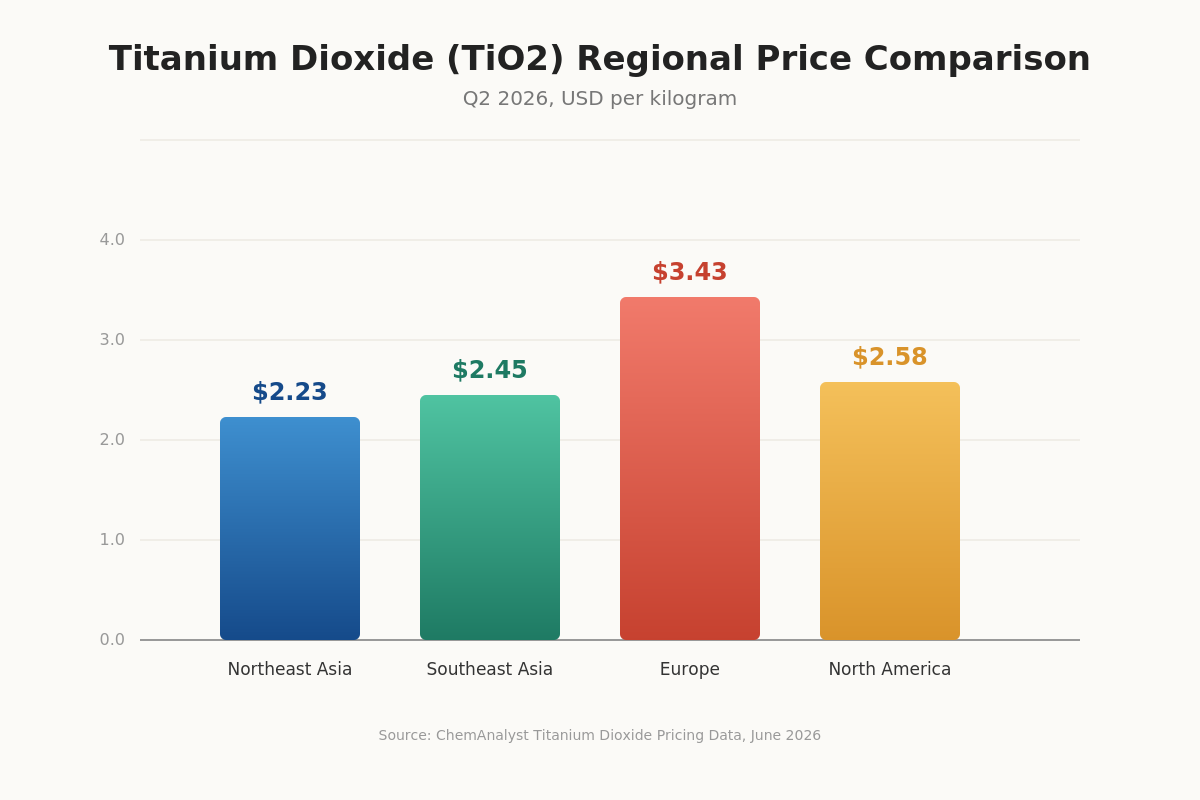

Titanium dioxide, the bellwether white pigment for the whole coatings supply chain, continued to show a “mixed” global picture through Q2 2026. Northeast Asian prices sat around US$2.23/kg, Southeast Asia around US$2.45/kg, Europe near US$3.43/kg, and North America around US$2.58/kg — with Europe and North America both down meaningfully year-on-year (roughly 7–10%) while Asian markets stayed comparatively firmer on steady coatings and plastics demand. In the U.S. specifically, ample inventories and softer construction and coatings demand kept spot prices under pressure into Q2, while feedstock costs (ilmenite, rutile ore) stayed relatively stable, limiting cost-side support for prices. (ChemAnalyst, Titanium Dioxide Pricing Data)

On the organic pigment side, raw material and energy costs remain the swing factor rather than feedstock scarcity. Several major coatings producers have pushed through further price increases this year — PPG, for example, announced a global increase of up to 20% earlier in 2026 — a reminder that even as commodity pigment prices soften in some regions, downstream formulators are still absorbing broader input-cost inflation from resins, solvents, and energy.

Takeaway for buyers: current market conditions favor active price benchmarking by region rather than assuming a single global trend — Asian buyers are seeing firmer pricing than their North American and European counterparts this quarter.

2. Company News

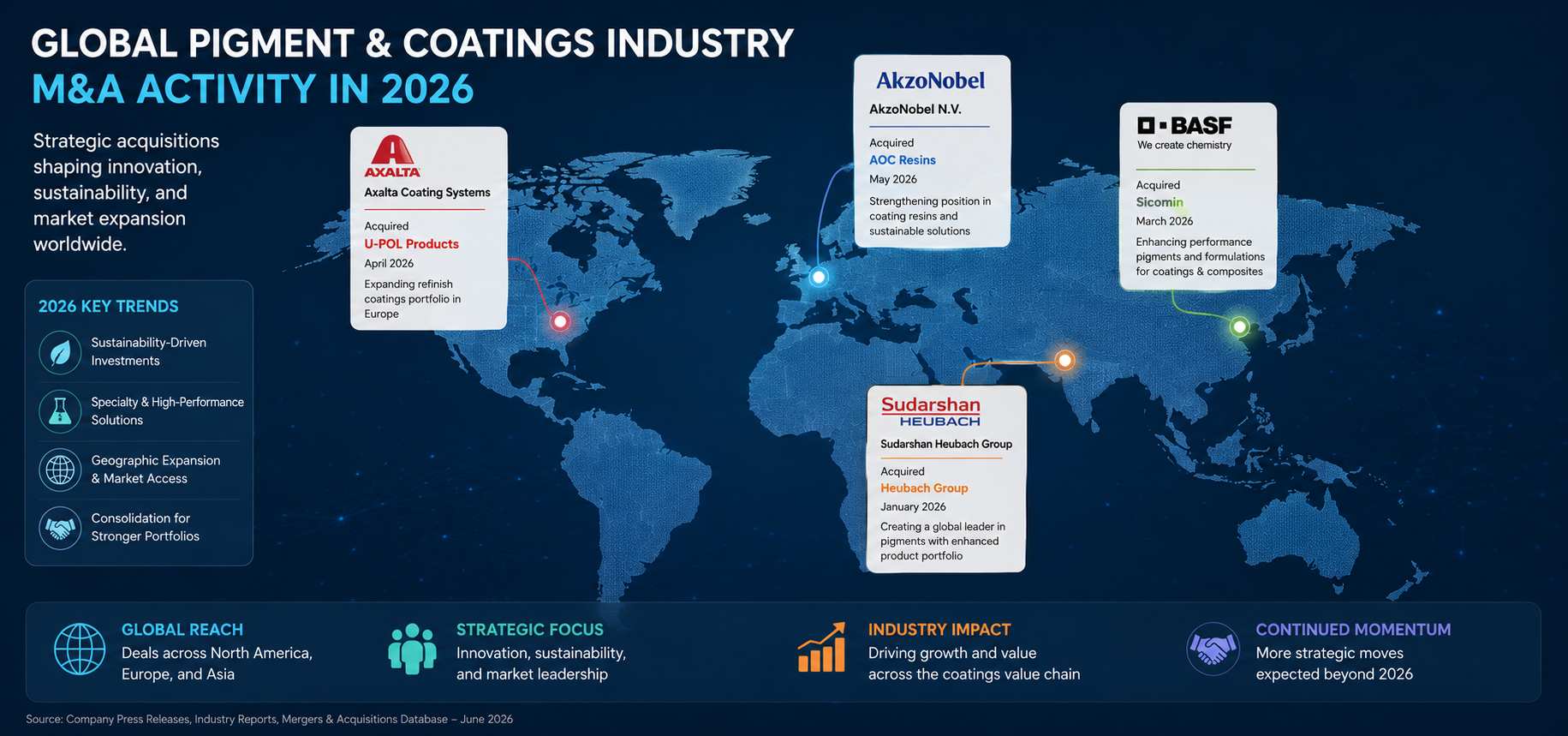

Consolidation remains the defining theme in coatings and pigments this year:

- AkzoNobel–Axalta merger continues moving toward its expected close in late 2026/early 2027, creating one of the largest global coatings groups, with AkzoNobel shareholders holding 55% and Axalta shareholders 45% of the combined entity. Analysts expect this to intensify pressure on PPG and Sherwin-Williams to pursue their own scale plays. (Chemistry World)

- BASF’s Coatings divestiture to Carlyle and the Qatar Investment Authority — covering BASF’s automotive OEM coatings, refinish coatings, and surface treatment businesses at an enterprise value of roughly €7.7 billion — is on track to close in Q2 2026, with BASF retaining a 40% equity stake in the new standalone entity. (Coatings World, M&A Roundup)

- PPG remains acquisitive, having completed its purchase of Ozark Materials (glass beads and pavement-marking materials) in April 2026, adding to a steady string of bolt-on deals in paints, coatings, and adhesion-related product lines.

- In the specialty pigments space, Sudarshan Chemical Industries’ acquisition of the Heubach Group continues to reshape the competitive landscape for organic and effect pigments, consolidating capacity that had previously been split across multiple mid-sized European and Asian producers.

The pattern across nearly every deal this year is the same: scale, portfolio simplification, and regional rebalancing — with several Western pigment producers continuing to explore shifting product lines toward the U.S. or Asia in response to rising European energy and compliance costs. (Coatings World, The 2026 Pigment Report)

3. Industry Events

The International Coatings Industry Expo (ICIE) in Guangzhou brought together coatings, pigment, printing ink, and raw material suppliers this month, continuing its role as one of the longer-running regional trade platforms in China (in its 18th edition, UFI-certified since 2012). Meanwhile, the industry is still digesting takeaways from PaintExpo 2026 in Karlsruhe (April), where AkzoNobel and other majors highlighted powder coatings innovation and where exhibitor space grew to roughly 89% of the prior edition’s footprint — a solid signal of continued investment in industrial coating technology despite broader macro uncertainty. (PaintExpo official news; Coatings World coverage)

4. Regulations & Sustainability

The EU regulatory picture shifted on two fronts this quarter:

- PFAS restriction proposal: ECHA’s Risk Assessment Committee (RAC) adopted its final opinion on March 3, 2026, and the Socio-Economic Analysis Committee (SEAC) closed its second public consultation on May 25, 2026, having drawn over 3,500 stakeholder submissions. Final RAC/SEAC opinions are expected by the end of 2026, with a European Commission draft restriction decision unlikely before Q1 2027 — and full adoption potentially not until 2029, following an 18-month transition period. For pigment producers, this remains a “prepare now, comply later” situation rather than an immediate compliance deadline. (ECHA official update)

- REACH 2.0 shelved: On April 27, 2026, the EU Environment Commissioner confirmed that the comprehensive revision of REACH (“REACH 2.0”) — which had been in development for nearly six years — has been shelved, citing a need for “regulatory certainty and predictability” for European industry. This gives manufacturers some near-term breathing room, though targeted restrictions (PFAS, SVHC updates) continue to expand on their own track. (European Commission, REACH Restrictions)

- U.S. pigment regulation: The Color Pigments Manufacturing Association (CPMA) continues to flag concerns with the EPA’s risk evaluation approach to Pigment Violet 29, warning that similar reasoning could extend to other pigments (CI Pigment Yellow 83, CI Pigment Yellow 65, CI Pigment Red 52) if left unchallenged — a live issue for any manufacturer selling into the U.S. market. (Coatings World, The 2026 Pigment Report)

Sustainability note: re-shoring interest is growing in the U.S. pigment sector, driven largely by rising European energy costs, carbon taxes, and REACH-related compliance burdens — though industry voices note Asia’s existing capacity overcapacity makes large-scale re-shoring from Asia less likely than from Europe.

5. Supply Chain & Logistics

Ocean freight is entering a seasonal inflection point. Freight forwarders describe June 2026 as “a critical transition period between the relatively stable first half of the year and the more volatile Q3 peak season.” Key regional trends:

- Trans-Pacific (China–U.S.) rates are expected to soften through the second half of June, with China-to-U.S. booking volumes still running roughly 30% below 2024 levels amid ongoing tariff uncertainty.

- Europe-bound freight is seeing moderate increases into June and July as summer and year-end inventory demand builds, compounded by periodic congestion at major ports (Rotterdam, Hamburg, Antwerp, Felixstowe).

- Red Sea rerouting remains the structural norm, not a temporary disruption — most carriers continue routing via the Cape of Good Hope, adding roughly 3,500 nautical miles per voyage. This keeps Asia–Europe rates elevated by an estimated 25–40% versus a “normal” Suez routing scenario, even as broader global freight rates sit well below their 2022 peak. (Xeneta, Red Sea Return & 2026 Contract Rates)

- Southeast Asia logistics remain comparatively strong, benefiting from trade diversification as exporters route more volume through the region.

Practical implication: for pigment buyers placing overseas orders, booking lead times of 4–6 weeks are increasingly advisable, particularly for Europe-bound shipments heading into Q3.

6. Upcoming Events (Next Month – July 2026)

- China International Coatings Expo (China Coatings Show) — July 15–17, 2026, Shanghai New International Expo Center. Organized by CNCIA, this year’s edition is expected to bring together 800+ exhibitors and over 100,000 visitors across 100,000 sqm, spanning powder coatings, green coatings, raw materials (including pigments and fillers), surface finishing, and smart manufacturing. This is one of the most relevant events on the calendar for pigment suppliers serving the coatings value chain, with dedicated forums covering automotive, construction, and military coatings applications. (CNCIA official show site)

7. Market Outlook

Heading into the second half of 2026, we expect:

- Pricing: continued regional divergence in TiO2 and commodity pigment pricing, with Asian markets holding firmer than Europe and North America; organic pigment prices likely to stay sensitive to energy and logistics costs rather than raw material scarcity.

- Consolidation: further M&A activity across both coatings majors (AkzoNobel-Axalta, BASF-Carlyle/QIA) and specialty pigment producers, likely accelerating capacity rationalization in Europe.

- Regulation: no immediate compliance deadlines from the EU PFAS restriction, but manufacturers exporting into the EU should begin substance-level exposure reviews now given the multi-year lead times involved in reformulation.

- Logistics: expect a bumpy Q3 as peak-season demand meets persistent Red Sea rerouting — buyers should lock in booking capacity early, particularly for Europe-bound cargo.

For Fineland Chem, this environment reinforces the value of our always-in-stock inventory model and flexible small-batch (1–2 bag) air shipping option, which allow customers to avoid getting caught out by regional price swings or peak-season freight bottlenecks.

This monthly brief is compiled from publicly available industry sources including Chemistry World, Coatings World, ECHA, PaintExpo, CNCIA, Xeneta, and ChemAnalyst. It is intended as a general market overview and does not constitute pricing, legal, or investment advice.